We live in uncertain times. I can’t think of any time in my life that that statement wasn’t true—we can never know the future. When it comes to investing and the stock market, predictions are pretty much worthless—since I bought my first stock at 28 years old, I’ve heard just about everything: don’t buy stocks now (whenever!), bonds are not really safe, Dow will hit 30,000, Dow will go down the tubes.

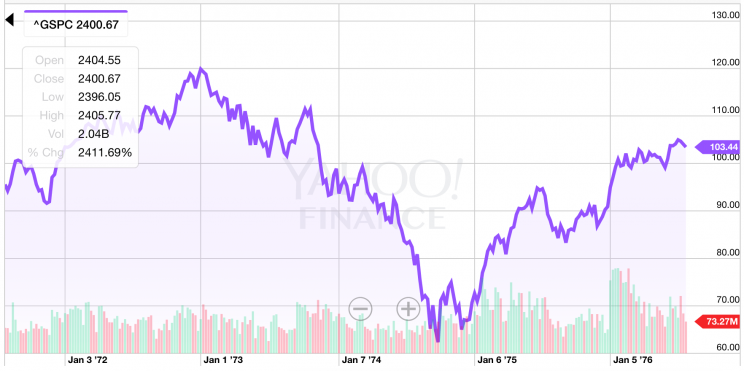

Most recently there was the expectation that the market would crash if the current incumbent was elected. Now there’s the worry that it will crash if he’s impeached. That might have some basis in fact. The S&P 500 declined about 50% from 1973 to Nixon’s resignation in August, 1974, according to this article. (While I remember Watergate, I wasn’t all that interested in the market at that time.) But as the article makes clear, a lot of other economic factors impacted that recession.

Analysis is perfect in retrospect. The best time to invest is usually some time before you did. Those of us who have faced challenging life circumstances—divorce, unemployment, illness—also know what it’s like to try to plan the future when that future seems radically altered. During those times, people often believe they have no future. But we always have a future (unless we’re dead); it’s just a different future than what we planned.

As I wrote in my client newsletter the day after the election (email me if you want a copy) we can take some protective steps no matter how uncertain our personal or political future seems.

Build an emergency fund

There’s just no substitute for this. In the middle of a crisis, it’s hard to increase it, so do your best to build it pro-actively. And if you’re in a situation where you need to draw it down, do so in the most frugal manner possible.

Improve your earning power

Get more education, build skills, get quality career counseling, and get out of the office and network. Think through ways to build a side income—gig economy, small business startup with LOW or no investment, whatever you can do.

Think through whether it really makes sense to quit your job to start a business: could you test the idea part time? Have you written a business plan and had someone else vet it?

Most important, guard against lifestyle creep. When you get a raise or earn extra, hold on to it! Use the improved earnings to build up your personal safety net.

Diversify your investments

For at least the past 10 years, I’ve been hearing how bonds are a terrible investment. During that same period of time, the Vanguard Total Bond Index mutual fund has had an annualized return of 4.17%–not great, but better than leaving it in your mattress, and beating inflation handily. People who had 40-50% of their portfolio in bonds during the 2007-2009 crash lost far less than those who were 100% in stocks. But in the doubling of the market after the crash, people who had abandoned stocks lost a ton of potential increases. Neither you nor I nor any of those genius active fund managers are going to make the right single bet on the market roulette wheel at any given time, so the safety move is to spread bets (investments) widely.

Take care of yourself

Making yourself sick is not going to cause one bit of change in an ex-spouse or corrupt politician. Eat well, see the doctor and dentist, exercise, and get a hobby—build yourself up and distract yourself with pleasurable activities to control how much you allow yourself to get worked up. People make very poor financial decisions under stress, so delay major decisions until you can think straight and get some expert input. On the other hand, don’t become paralyzed—not to decide is to decide (Harvey Cox)—and avoiding decisions for very long periods mean you’ve lost control over your own life.

Join something bigger than yourself

Times of turmoil are great times to join a group, take a class, do volunteer or advocacy work. You’ll feel less alone, find ways to get input on personal decisions, and learn how to exert influence on issues that concern you. Studying history, learning to draw, joining a book or investment club, or becoming active in a political group can all impact your personal success, life satisfaction, and ability to envision a future you can plan for.

In his most recent newsletter, former Wall Street Journal columnist Jonathan Clements observes (correctly) that most of us will never be fabulously wealthy, that we should stop feeling bad about that, and that this bizarre cultural belief leads people to be discontent with any achievement, and to chase hucksters who promise self-transformation and lunatic investment schemes. (

In his most recent newsletter, former Wall Street Journal columnist Jonathan Clements observes (correctly) that most of us will never be fabulously wealthy, that we should stop feeling bad about that, and that this bizarre cultural belief leads people to be discontent with any achievement, and to chase hucksters who promise self-transformation and lunatic investment schemes. (